Canada Visitor Visa Bank Balance Myths, Busted (2026)

Last reviewed: 14 May 2026 · Verified against current VFS Global India fees

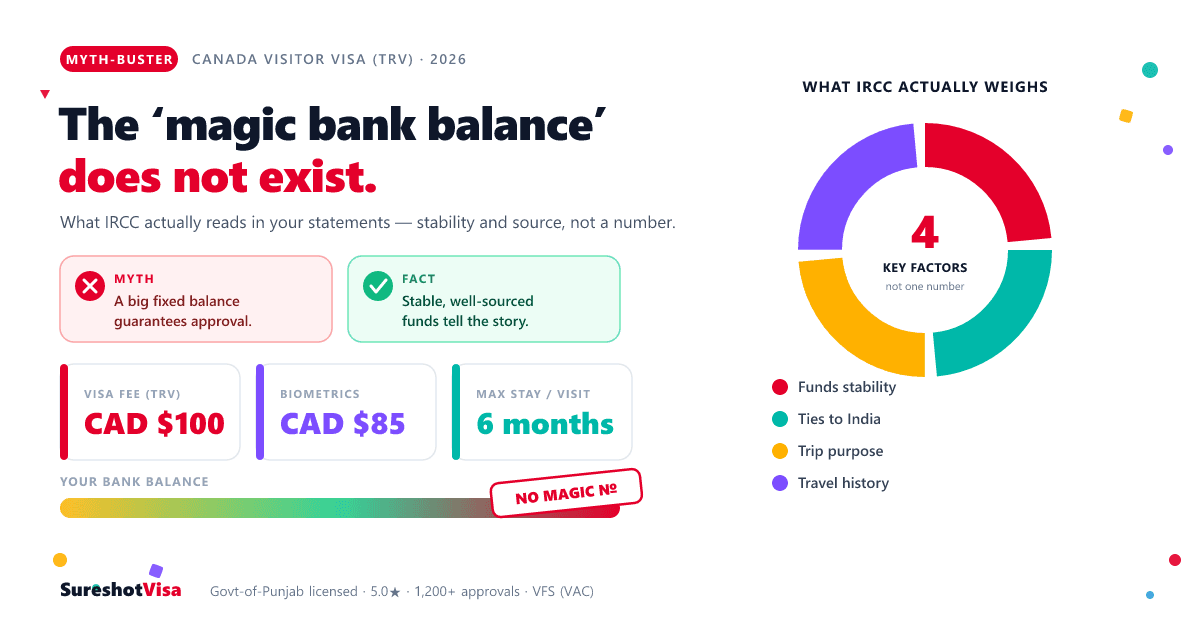

There is no magic bank balance number for a Canada visitor visa. Six myths against what IRCC officers actually read in your six-month statements.

There is no magic bank balance for a Canada visitor visa. None.

"Show ₹10 lakh and it's done." "Park an FD and relax." Every WhatsApp group has a number, and every number is made up. Here is what an IRCC officer actually reads in your statements — six myths, put against the record.

IRCC has never published a minimum. That is the whole point.

Ask ten agents what balance "gets" a Canada visitor visa and you will get ten confident, different numbers. Ask IRCC, and you get silence — because no such figure exists.

The official requirement for a Temporary Resident Visa (TRV) is proof of financial means: sufficient funds to support your stay in Canada. No fixed minimum — but strong proof expected. What is fixed is the evidence format: bank account statements for a minimum of six months, showing the bank's name, your name and address, monthly balances and transactions. Not a screenshot of today's balance. Six months of financial behaviour.

That distinction is where most refusals over "funds" actually come from. The officer is not weighing your account against a secret threshold. They are reading a six-month story and asking whether it is stable, explainable, and consistent with the rest of your file. A large share of Indian TRV refusals cite funds and weak ties — and most of that is avoidable, because the problem is usually presentation, not poverty.

For the full document list, fees and process, our Canada tourist visa guide covers the mechanics. This piece is only about the money myths. Let's break them.

The myth board

The most repeated number in the market — and it appears in no IRCC rule anywhere.

There is no official minimum. You need enough to credibly cover your trip — flights, stay, expenses — with stability over the last six months. A modest, steady balance that matches your income beats a fat balance that appeared last Tuesday. We assess the right figure for your specific itinerary in the ₹499 report.

The classic "show money" play — borrow, deposit, print, return.

Officers read transactions, not just totals — that is precisely why IRCC demands six months of statements with monthly balances and transactions visible. A sudden large deposit with no documented source is one of the most frequent refusal reasons for Indian applicants. If a genuine large credit exists — property sale, maturity, bonus — it is fine, provided the source is documented in the file.

So people attach statements and skip the ITRs.

The officer cross-checks whether your savings are possible on your declared income. ₹15 lakh in the account of someone with no ITRs and no visible salary credits raises questions, not confidence. Strong files pair statements with ITRs, salary slips or business proof so income and savings line up. Alignment is the test — not altitude.

Money answers everything, supposedly.

Ties — a job with approved leave, a running business, property, family who depend on you — are the single biggest factor in TRV approvals for Indians. Funds prove you can afford the trip; ties prove you will come back from it. An officer unconvinced you will leave Canada refuses a millionaire as readily as anyone else.

Half true — which is what makes it dangerous.

Immediate family already in Canada can be read as immigration intent — a documented refusal ground. A properly worded invitation letter stating your host's PR/citizen status, the relationship, your stay plan and who pays helps; a vague one that contradicts your file hurts. The fix is a strong return-incentive narrative with ties evidence, not hiding the relative.

So the next application arrives with a bigger, newer lump sum. And fails again.

The refusal letter's tick-box rarely tells the whole story. GCMS notes — the officer's actual internal reasoning — often reveal the real ground was purpose, ties, or an unexplained deposit, not the amount. Reapplying with "more money" against the wrong problem burns another fee. Our Canada refusal-recovery service starts from those notes and rebuilds against the true reason.

Five things IRCC actually reads in your statements

Bank name, your name and your address, printed on the statement itself. Minimum six months of it. A statement that fails the format test undermines everything on it — this is the easiest box to get right and a surprisingly common one to get wrong. Our bank-statement guide for Canada covers the exact spec.

Monthly balances across six months. Steady, or gently rising, reads as savings. A flat line that spikes the week before submission reads as staging.

Salary credits that match the employment letter. Business inflows that match the GST story. Regular life — rent, school fees, groceries. Real accounts look lived-in.

Each big credit gets one silent question: where did this come from? If the answer is in the file — sale deed, FD maturity, documented gift — the question closes. If it isn't, it can close the application instead.

Statements are read beside your ITRs, your stated purpose, your itinerary and your invitation. One inconsistent number — a trip your savings can't plausibly fund, or income your account never received — is worth more to a refusal than any balance is to an approval.

The government cost is the same whatever your balance: CAD $100 visa fee plus CAD $85 biometrics — about CAD $185, roughly ₹11,500 — paid online to IRCC, plus small VFS charges in India. Biometrics stay valid ten years. None of it is refunded on refusal, which is the financial argument for filing it right the first time.

What "enough money" really means

Strip the folklore away and the funds test is three questions. Can this applicant afford this specific trip? Is the money genuinely theirs — stable, sourced, consistent with income? And does the financial picture support a temporary visit rather than a one-way move? Answer all three on paper and the balance itself becomes almost boring.

That is how we build files at SureshotVisa: six-month statements presented properly, a source-of-funds note for anything unusual, ITRs and income proof aligned, ties evidenced, and an invitation that matches rather than contradicts. Processing typically runs 30–60 days, so the file gets one chance to speak for you while you wait. The full walkthrough — documents, funds, ties, refusal patterns — lives on our Canada visitor visa from India page, and our filing service is ₹14,999 all-in, itemised on the pricing page.

Bank balance FAQs, answered straight

Is there a minimum bank balance for a Canada visitor visa from India?

No — IRCC publishes no minimum figure. You must show sufficient funds for your specific trip, evidenced by at least six months of bank statements with a stable balance. A steady account that matches your income matters far more than any headline number.

How many months of bank statements does IRCC want?

A minimum of six months. The statements must show the bank's name, your name and address, monthly balances and transactions. Officers read the pattern across those months, not just the closing balance.

Will a large deposit just before applying get my visa refused?

An unexplained one very often will — insufficient or unexplained funds is a standard refusal ground. If the deposit is genuine, document its source (sale, maturity, bonus, gift) in the file. Sourced money is an asset; mystery money is a liability.

Do I need ITRs and salary slips if my balance is already strong?

Yes. The officer checks whether your savings are consistent with your declared income, and a balance your income cannot explain invites doubt. ITRs, salary slips or business proof make the money credible rather than merely large.

Does having family in Canada help or hurt my application?

Both are possible. A well-drafted invitation letter from a host with clear PR/citizen status strengthens a family-visit file, but close family in Canada can also be read as immigration intent. The counterweight is strong, documented ties to India showing you will return.

What are GCMS notes and when should I order them?

GCMS notes are the officer's internal reasoning behind a decision on your file. After a refusal, they reveal the real ground — which is frequently not the tick-box on the letter — so the reapplication targets the actual problem. We use them as the starting point of every refusal rebuild.

Can SureshotVisa guarantee my Canada visitor visa?

No — and be wary of anyone who says otherwise. The decision rests entirely with IRCC. What we control is the quality of the file: funds presentation, source documentation, ties and purpose, prepared by people who do this daily.

Get your funds story read the way an officer will read it.

SureshotVisa is a Government-of-Punjab licensed consultancy (Lic. No. 849/DC/PTA/PLA/LC-3/2024). For ₹499 we review your profile — statements, income, ties, purpose — and give you a written visa-possibility report with the honest odds and the exact fixes, before you spend the IRCC fees. Credited in full if you file with us. We prepare the file; IRCC alone decides it.

+91 91155 80911Prefer WhatsApp? The green button at the bottom of your screen reaches the same desk.

Notes on sources. Filed 04 July 2026. Requirements and fee figures reflect IRCC and VFS Global India published information (TRV CAD $100, biometrics CAD $85, ≈ ₹11,500 combined) as of the publication date; fees and rules change without notice — verify on canada.ca before applying.

This article is for information only and does not guarantee a visa. Every application is assessed on its own merits, and the final decision rests solely with IRCC. Anyone promising a guaranteed Canada visa is selling something no one can deliver.

© 2026 Sureshot Visa · A brand of Pro Lifeset Overseas Pvt Ltd · Patiala, Punjab

Need help?

We'll handle your visa file end-to-end.

Documents, VFS slots, embassy filing — by a licensed consultant.

We answer within 5 minutes

Full Country Guide

Canada Visa from India — fees, documents, processing time

Everything you need on one page: VFS centres, visa types, fee breakdown, doc checklist.

Written by

Narinder ChahalFounder, SureshotVisa · B.Tech, Computer Science (2008)

Narinder Chahal founded SureshotVisa with a simple belief: a visa file should be clear, honest and backed by strong documents. After moving to Canada in 2014, he has helped Indian and international applicants understand visa filing, refusal concerns, document gaps and immigration-related issues.

Full profileRelated Guides

Can You Take Your Dog to Canada from India? The 2026 Pet Guide

Yes — your dog can come to Canada, and the paperwork is simpler than you fear. The one document CFIA cares about, the airline choice that trips people up, and the timeline to start now.

Read guide

Pinni, Achaar & Parshad to Canada: What You Can Actually Pack (2026)

Yes, you can carry many Indian foods to Canada — but the fine is for NOT declaring, not for the food. The green / amber / red guide to packing your maa-ke-haath sweets without a CA$1,300 surprise.

Read guide

Canada Visitor Visa Refused? The Honest 2026 Reapply Guide for Indians

Your Canada visitor visa was refused. Now what? A clear, India-first 2026 guide to reading your refusal, getting GCMS notes, and deciding whether to reapply, request reconsideration, or seek judicial review.

Read guide

Canada Study Visa Refusal Reasons 2026: The Student File MRI

Canada study visa refused in 2026? A visual diagnostic — SOP heatmap, course-fit bridge, funding pipeline, PAL/TAL gate, study-gap logic and a reapplication self-audit.

Read guide